[ad_1]

By 2023, there will be over 350 million connected cars on the road. What can the insurance industry do about it? It turns out that quite a bit, as automotive companies, introducing the latest technological advances, are enabling new ways to mix driver behavior. This is of great importance in the context of creating offers, but not only. At stake is to maintain the position and competitiveness in the field of motor insurance.

The automotive and car insurance industries are changing

The automotive market is already experiencing changes driven by innovative technologies. More often than not, these are based on the software-defined vehicle (SDV) trend.

If the vehicle is equipped with embedded connectivity, it is able to provide very detailed vehicle and driver behavior data, such as:

● sudden acceleration or braking,

● taking sharp turns,

● peak activity times (nighttime drivers are more vulnerable),

● average speed and acceleration,

● performing dangerous maneuvers.

BBI & UBI and ADAS

Behavior-based (pay-how-you-drive) and usage-based insurance – UBI – (pay-as-you-drive) are the future of car insurance programs. Meanwhile, as vehicles become smarter, more connected, and automated, insurers evaluate not only the driver’s behavior but also the car s/he is driving. This evaluation takes into account, among other things, the amount of advanced driver assistance systems (ADAS) that affect the safety of the vehicle’s occupants.

Autonomous vehicles

And Deloitte analysts note that self-driving (AV) cars, which are an interesting novelty now but will in time be a standard on par with human-driven vehicles, are also likely to force fundamental changes in insurers’ product ranges, as in the risk assessment, pricing, and business models.

Connected cars

Change is already happening, and it will become even more pronounced in the years ahead. IoT Analytics predicts that by 2025, the total number of IoT devices worldwide will exceed 27 billion. Plus, experts predict that there will be 7.2 billion active smartphones and more than 400 million connected vehicles on the road during the same period.

This all clearly shows that we are in an entirely different reality than we were just a few or a dozen years ago. Car insurers need to understand this if they want to maintain their foothold.

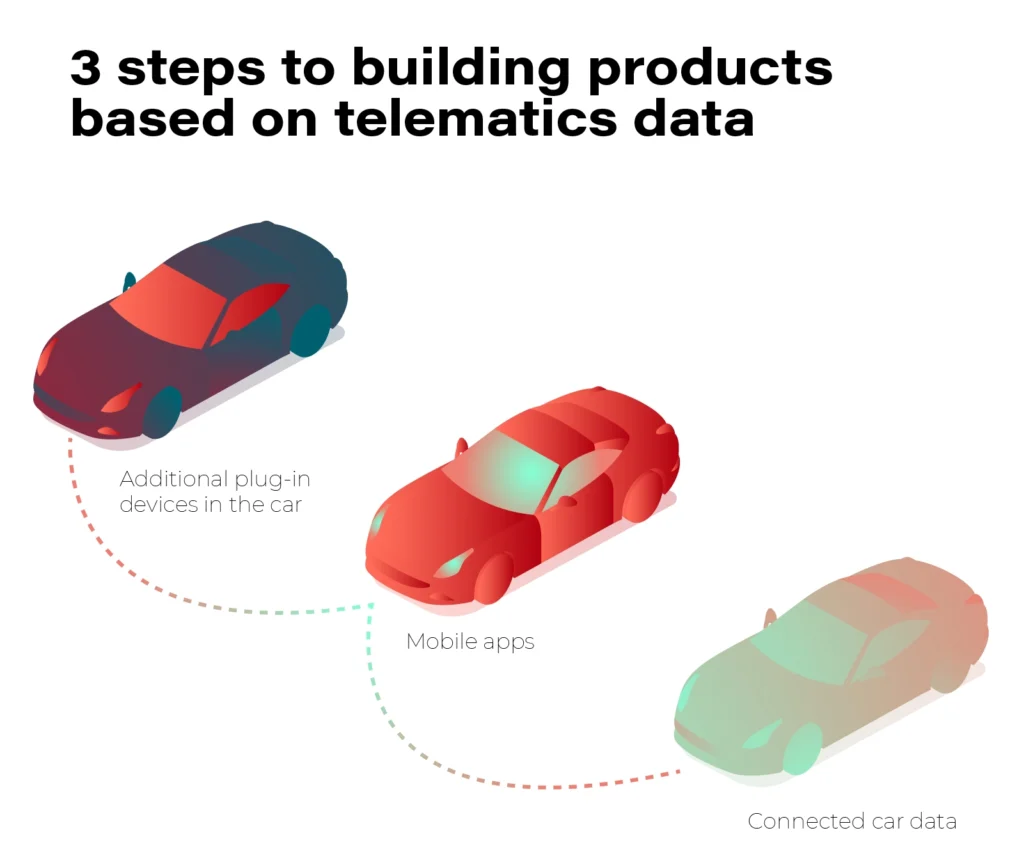

Telematics technologies are an obvious step into the future of the insurance industry

Insurance companies have been offering usage-based and behavior-based products for years based on data from either additional devices or mobile apps. This is a fast-growing product area since the UBI market is predicted to be worth more than $105 billion in 2027, up 23.61% annually.

The best position in this arena is attained by businesses that started investing in telematics technology early and now can take pride in well-developed telematics products.

We are talking about brands such as State Farm®, Nationwide, Allstate, and Progressive. Yet at the same time, companies that deemed telematics a passing trend and therefore didn’t invest in it lost a very large amount of market share. The result? Now they have to catch up and race to keep up with the competition.

TSPs understand the potential of connected vehicle data

Insuring companies are not the only ones who recognize the importance of implementing their telematics-based solutions. Telematics services providers understand that value as well, so they invest in building out new capabilities of their products.

This is the case with GEICO, the second-largest auto insurer in the U.S. (right after Progressive). As Ajit Jain, vice president of Insurance Operations at Berkshire Hathaway claims: GEICO had clearly missed the business and were late in terms of appreciating the value of telematics. They have woken up to the fact that telematics plays a big role in matching rate to risk. They have a number of initiatives, and, hopefully, they will see the light of day before, not too long, and that’ll allow them to catch up with their competitors, in terms of the issue of matching rate to risk.

Telematics companies see potential in partnering with the insurance industry

Insurance companies are not the only ones who recognize the importance of implementing new data-driven technology solutions. The relationship is two-way, as telematics industry representatives, in turn, are willing to invest in collaboration with insurers and put the customer from this market sector first.

For example, Cambridge Mobile Telematics (CMT), the world’s largest telematics provider, has recently announced the expansion of its proprietary DriveWell® telematics platform to networked vehicles. Their flagship software has previously collected sensor data from millions of IoT devices, including smartphones, tags, in-car cameras, third-party devices, etc. From now on, that scope continues to expand by specifically including connected vehicles to create a unified view of driver and vehicle behavioral risk.

This synergy of all acquired data is mainly dedicated to customers in the auto insurance industry, who gain insight into what is happening on the road and behind the wheel. As Hari Balakrishnan, CTO and founder of CMT explains: There is a wave of innovative IoT data sources coming that will be critical to understanding driving risk and lowering crash rates. CMT fuses these disparate data sources to produce a unified view of driving.

Current UBI solutions can be flawed

Existing methods of data collection for insurers also rely on modern technologies, but these can be unreliable. All three methods have their drawbacks: devices plugged into the On-Board Diagnostic (OBD) system, smartphone apps and tags stuck to the windshield.

The first method provides insight into the driver’s precise behavior data, downloaded directly from the engine control module (ECM). Weaknesses? The fact that OBD-II devices are limited to the data found in the ECM, for example, while those from other vehicle components remain inaccessible.

In this respect, mobile apps are certainly better, providing insurers with a simple way to launch their own telematics-based program. . In addition, data is collected every time the user drives the vehicle. The disadvantage, however, is that the software does not connect directly to the vehicle’s systems. Therefore, the data points are subject to a margin of error, and it also happens that the automatic driving recognition fails and includes in the scoring journeys as a passenger in another car, for example.

Bluetooth-based tags, which is the last solution described here, are installed on the vehicle’s windshield or rear window. Like mobile apps, the tags have no direct connection to the vehicle’s systems and are therefore prone to bugs.

The conclusions are obvious

Thus, there is a lot to suggest that if an insurer is looking for truly reliable technology, it should opt to use embedded telematics, or data. This is what enables dynamic and, above all, unconditional data collection to reliably assess the risk associated with individual clients.

The data sent by connected cars is more accurate, more detailed, and in much larger quantities compared to other solutions. And this allows insurance companies to better understand customers and their behavior and, based on this information, offer products that are better suited to their needs, as well as more profitable.

Industry insiders don’t need much convincing about the advantages of telematics and connected cars over other driver data collection solutions. Data from cars connected to the network are instantly obtainable. Of course, you can enrich it and give it context by using information from smartphones, but in most cases, it is not even necessary. So why invest in something unreliable, which by definition has vulnerabilities and does not meet 100 percent of your needs, when you can opt for a more comprehensive technology that offers more features right from the start.

Considerable importance of connected car data for the insurance industry

Connected car data is the subsequent step in building the ultimate telematics-based products. It is acquired without the need to install additional components. All it takes is a vehicle user’s consent to use the data, and then the insurance company obtains the data directly from the OEM.

The information obtained from UBI vehicles can be used successfully and all stakeholders benefit: insurers, as they gain a better understanding of their customers and can better assess risk; OEMs, as it allows them to monetize the data; and finally consumers, who receive a better, more personalized offer this way. J.D. Power points out that 83% of policyholders who had positive claims experience renewed their policies, compared to only 10% who gave negative reviews.

In addition, such reliable data serves not only to improve the profitability of an insurance portfolio, but also to improve road safety. Insurers can offer incentives that will encourage their customers to continuously improve their driving style and increase their care for themselves and other road users.

Even now, market leaders who understand the value of investing in innovation are offering their customers the opportunity to share data from connected cars for UBI/BBI purposes. One example is the State Farm® brand, which offers discounts based on driving behavior. The driver’s on-the-road behavior ( sharp braking or no braking, rapid acceleration, swift turns) and driving mileage are automatically sent to the data manager after each trip, so be sure to enable data sharing and location services on your saved vehicle. This information is used to update your Drive Safe & Save discount each time you renew your policy. The safer you drive, the more you can save.

Likewise, Ford Motor Company is increasingly shifting toward using driver data in UBI programs based on connected vehicles. To that end, the automotive giant has partnered with a mobility and analytics brand. Their joint project is expected to empower drivers with more control over how much they pay for their car insurance. Drivers can voluntarily share their driving data from activated Ford vehicles with Arity’s centralized telematics platform, and it will then be delivered via Arity’s API. Drivesight® to insurers. The obtained risk index can be used to price auto insurance by any participating insurer.

Currently, connected cars are only one option, as many insurance companies are still using, for example, mobile applications in parallel. However, we can already see that the trend of using CC data is present on the market and the number of companies offering such an option to their clients will grow. This is something to be reckoned with.

Significant benefits

For insurers, the benefits are tangible. According to Swiss Re, with 20,000 claims handled per year, the average savings after implementing the above technologies amounted to 10-30 USD per claim.

Telematics also helps to curb so-called claims inflation. Increasingly advanced vehicles are equipped with complex components, which can be costly to replace. Fortunately, today’s insurer has the ability to create its own strategy based on the changing cost of spare parts and damage history for major car models. This enables them to develop new pricing that includes inflated compensation costs.

The sooner, the better

Leveraging data and analytics based on artificial intelligence is guaranteed to drive growth. Expanded sources of information improve the customer experience and help streamline operational processes. The benefits are thus evident across the entire value chain. We can confidently say that never before in history has technology been so intertwined with the insurance industry.

That’s why all insurance companies should start working on incorporating connected car data into their programs now. The sooner they do, the better positioned they will be when such vehicles become mainstream on the road. After all, the share of new vehicles with built-in connectivity will reach 96% in 2030.

That’s what Evangelos Avramakis, Head Digital Ecosystems R&D, Swiss Re Institute Research & Engagement advises insurance companies to do: Starting small then scaling fast might be a good strategy (…) There is so much you can do with data. But you need to take a different approach, depending on whether you want to improve claims processing or create new products. Conversely, this is what Nelson Tham, eAdmin Expert Asia, P&C Business Management, thinks about implementations: Whenever an SME thinks about digitalization, it intimidates them. But it need not be the case if we start small. They can begin by reviewing their internal processes, see how data flows, turn that into structured data, then analyze this data for more meaningful insights.

How the insurance industry should approach the subject?

Insurers should start by answering key questions like: where connected car data will deliver the most value for my business? What internal capabilities do we have and need? Do we have the required infrastructure, process and skills to leverage connected car data? What investments in technology are necessary to deliver on our goals?

Lastly, they need to consider whether they can better and faster achieve those goals by building required capabilities in-house or working with partners.

A good business and technology partner for the insurance industry is fundamental

Using connected car data is not that straightforward. It requires know-how and the right technology background, as well as finding the right partner to collaborate with.

A well-matched partner will help change the current operating model, by combining automotive and technology competencies and at the same time understanding the specifics of the insurance industry. Some processes simply have to be carried out in a comprehensive and holistic way.

At GrapeUp, we help implement new approaches to an existing strategy. Operating at the intersection of automotive and insurance, we specialize in the technologies of tomorrow. Contact us if you want to boost your business performance.

[ad_2]

Source link

More Stories

7 Reasons Why Branded or High Quality Products Are So Important to Buy

Living In A Disposable Society – An Addiction To Junk

Latest Mobile Phones 2010 – Outlandish Devices of Modern Era